Don’t Carry Credit Card Balance

Don’t Carry Credit Card Balance

Oh, Instant Gratification

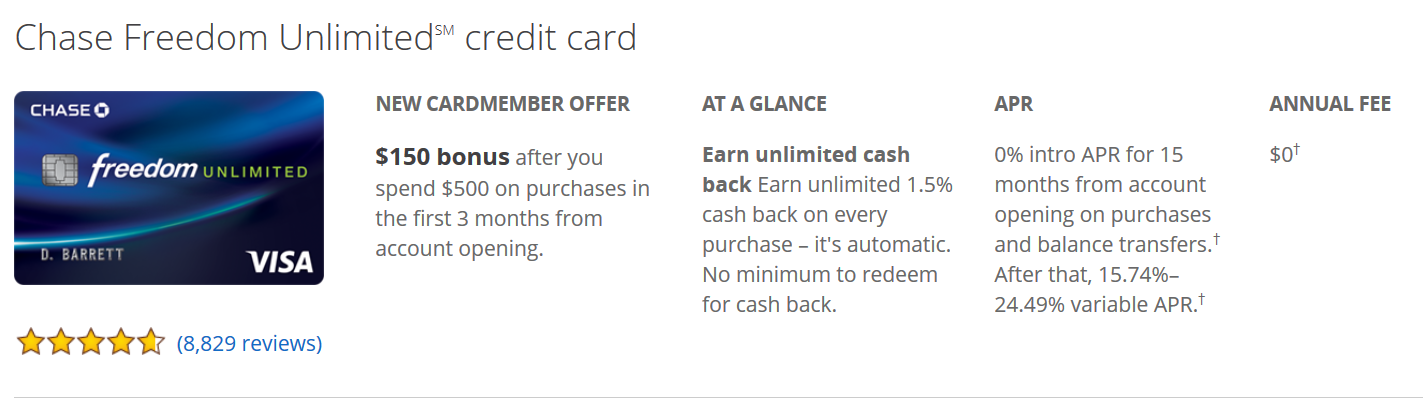

Credit is so widely available that it is hard to pass up using it to satisfy our urge to instantly gratify our desires for stuff. I’m not knocking buying stuff on credit at all especially if you can afford it, and by afford it, I mean pay off the balance in full each month with either savings or monthly cash-flow. If not, you should tread lightly using credit for your discretionary spending because the Annual Percentage Rate (APR) on that credit is usually pretty high. Take for example some of the credit cards I recommend like the Chase Freedom Unlimited or Chase Sapphire Preferred, they have 15.74% – 24.49% variable APR. These APR don’t get much lower under other credit cards either.

Typical Interest Charge Calculation

The typical way in which credit cards charge interest is like below:

- (APR ÷ 365) = Daily Periodic Rate (DPR)

- (DPR × 31) × balance = Interest charge

(((15.74 ÷ 100) ÷ 365) × 31) × $1000 = $13.37.

Your new balance is $1013.37. You might say oh $13.37 is not that bad, but look what happens next month if you weren’t to pay down this balance quickly

- (((15.74 ÷ 100) ÷ 365) × 31) × $1013.37 = $13.54

- (((15.74 ÷ 100) ÷ 365) × 31) × $1026.91 = $13.72

- (((15.74 ÷ 100) ÷ 365) × 31) × $1040.63 = $13.91

- (((15.74 ÷ 100) ÷ 365) × 31) × $1054.54 = $14.10

- …

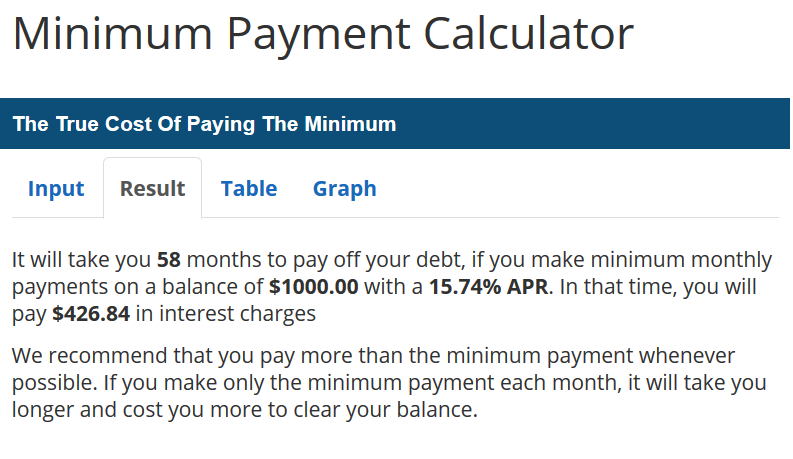

The interest on the balance begins to compound at this high rate and, in addition, if you continue to add to the balance, this can get out of hand extremely quick. Paying the minimum of $25 can mean paying $426.84 in interest over 58 months. No bueno?!

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Minimum Payment Calculator |

Wealth Transfer

The banks are making exorbitant amount of money when you slip up even a little. Contrast these rates by the 9.8% average annualized total return of the S&P 500 over the last 90 years. Even if you were eager to do something else which I suggest which is invest, it would make little sense to do so because the interest rates on credit would outpace gains from stock market or other investments as well. Unfortunately, the wealth which you could be building for yourself and your family is being transferred to JP Morgan Chase, Citi, Wells Fargo, and their shareholders, etc.

Start Move Towards Credit Balance Reduction

So if you are in this situation, it is best to have narrow focus to get quickly from under large credit card balances and then continue to keep balances at zero or payable within 3 months. If this cannot be done so easily, here are a few suggestions I heard have worked or I know are possible to get moving in the right direction:

- Call the lender and explain your situation and ask for lower rate.

- If your credit score (get free credit score here) is in the high 680’s and above, consider doing a balance transfer using a 0% promotional rate. You can find offers here.

- Escalate paying much more than minimum payment on credit card balances and more frequently as banks typically use daily average balance, so keeping the averages low can mean less interest gets charged. Try paying weekly or bi-weekly in billing cycle, instead of monthly.

- Don’t add new purchases to a credit card with an already large balance.

- Try using service like Debitize (see my blog @ Debitize on personal experience using this service)

In Closing

I don’t advocate cutting up your credit cards once you get out of debt, but I do suggest using credit responsibly for mostly non-discretionary spending for things you have to pay monthly for anyway like cell phone, utilities, food, insurance, and the like when you have some sort of incoming cash-flow. Think twice about putting discretionary spending like vacations, shopping, eating out and the like on credit cards if you know you don’t have the money or will not have the money to pay for it in less than 3 months because you see the damage that can happen in short period of time for just $1000 balance. Now, I gave you fair warning, beware carrying credit card balances!

Please provide feedback or questions pertaining to this blog post by leaving a comment below. Also please be sure to share this content with your friends and family. I thank you in advance.

Please provide feedback or questions pertaining to this blog post by leaving a comment below. Also please be sure to share this content with your friends and family. I thank you in advance.